My Three Cents

Ken Makovsky

Monday, October 24, 2016Can Wells Fargo’s Reputation Be Saved?

The recent revelation that Wells Fargo bank branches opened millions of fake customer accounts and 500,000+ credit cards that customers didn’t ask for was actually not “new” news.

![]() In fact, it was first reported by the Los Angeles Times nearly three years ago in “Pressure-Cooker Sales Culture Comes at a Cost” — based on a tip by a bank employee and interviews with more than two dozen current and former Wells employees and customers, as well as review of internal bank documents and court records. You may be interested in the whole denouement of this development in the Columbia Journalism Review, which recently profiled the investigative reporter on this story, E. Scott Reckard.

In fact, it was first reported by the Los Angeles Times nearly three years ago in “Pressure-Cooker Sales Culture Comes at a Cost” — based on a tip by a bank employee and interviews with more than two dozen current and former Wells employees and customers, as well as review of internal bank documents and court records. You may be interested in the whole denouement of this development in the Columbia Journalism Review, which recently profiled the investigative reporter on this story, E. Scott Reckard.

Behind the scenes of the nation’s leading bank in selling add-on services to its customers were, it was reported, ethical breaches, customer complaints, labor lawsuits, and frightened employees under relentless pressure to sell, under threat of losing their jobs. “To meet quotas, employees have opened unneeded accounts for customers…forged client signatures on paperwork… begged family members to open ghost accounts… talked a homeless woman into opening six checking and savings accounts with fees totaling $39 a month.”

But the story only became national news this past September when the bank, one of the country’s most sound and successful financial institutions, received a hefty regulatory fine ($185 million) from the Comptroller of the Currency, the Consumer Financial Protection Bureau, and the Los Angeles City Attorney.

Things quickly went downhill from there. Wells Fargo CEO John Stumpf was chastised by Senator Elizabeth Warren for “gutless leadership.” She insisted he resign and face criminal investigation at a September 20th Senate Banking, Housing and Urban Affairs Committee hearing (Source: Forbes). Committee members weren’t satisfied with his apology. He was called out for lack of executive accountability and pinning the blame on branch employees – 5,300 were fired.

Before Mr. Stumpf was to face the House Finance Committee a week later, the bank’s board moved to rescind his pay and to have him forfeit $41 million in unvested equity awards, according to the Wall Street Journal. In addition, the recently retired head of community banking who oversaw retail banking, Carrie Tolstedt, forfeited $19 million in unvested equity awards.

It came as no surprise when, on October 12, two days before the company’s latest quarterly earnings announcement, Wells Fargo announced Mr. Stumpf’s retirement, effective immediately. (He was replaced by longtime CFO Timothy Sloan, who had been quoted in the LA Times three years ago, in the story that broke the news, “I’m not aware of any overbearing sales culture.”)

Was it a case of senior management ignoring clear signals of a problem? Executive complacency because the numbers were good? Internal communications problems? A flawed corporate culture in which employees were afraid to speak up? Or did leadership forget the qualities that made it such a successful financial institution?

Regardless of the root cause or causes, one thing is clear: the organization was exceptionally slow to address what has become a potential reputation-killer with its stakeholders. Consider this: Wells Fargo had three years to address the problematic sales practices revealed by the LA Times. The organization evidently did nothing, and was not prepared once everything hit the fan. And when it received a regulatory fine in September, it was in denial, persisting for several weeks until taking action.

One of the cardinal rules of crisis management is, if you’re wrong or made a mistake, admit it quickly, apologize and create a plan to fix it. The longer it goes unaddressed, the more the reputation damage.

It’s a tragedy that leadership risked squandering its reputation by not acting three years ago. Good reputations are hard to earn in today’s financial industry landscape. Today, eight years after the 2008 global financial crisis, its impact remains present in the minds and balance sheets of consumers and industry alike, according to the Makovsky 2016 Wall Street Reputation Study. The institutions recognize this; 86% of executives we surveyed said the 2008 financial crisis still has a major effect on perception of their companies. “Public perception of industry” was the top negative issue affecting reputation in the past year.

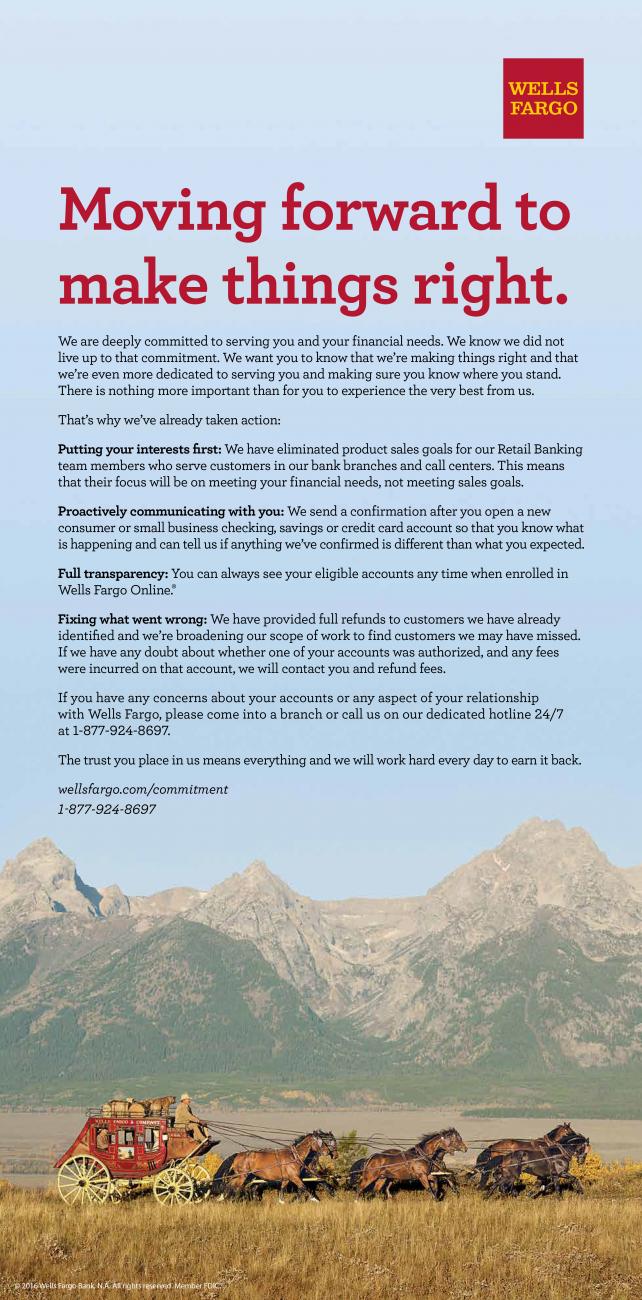

Longtime Wells Fargo CFO Timothy Sloan, now the newly appointed CEO, seems to be moving quickly to turn the tide. By mid-October, the company began to reintroduce marketing with an ad campaign, “Moving forward to make things right,” explaining what it is doing to change the culture, as reported to AdAge. We wish Wells Fargo the best in mending the reputation damage: its future will heavily depend on its success.